By A Mystery Man Writer

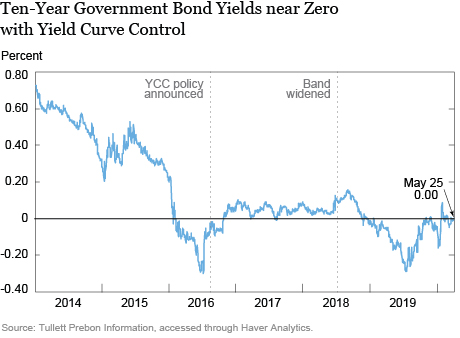

In September 2016, the Bank of Japan (BoJ) changed its policy framework to target the yield on ten-year government bonds at “around zero percent,” close to the prevailing rate at the time. The new framework was announced as a modification of the Bank's earlier policy of rapid monetary base expansion via large-scale asset purchases—a policy that market participants increasingly regarded as unsustainable. While the BoJ announced that the rapid pace of government bond purchases would not change, it turned out that the yield target approach allowed for a dramatic scaling back in purchases. In Japan’s case, the commitment to purchase whatever was needed to keep the ten-year rate near zero has meant that very little in the way of asset purchases have been required.

What the end of Japan's yield curve control experiment means for markets

The global implications for a shift in Japan's yield curve control

Morning Bid: Yield curve control morphs

:max_bytes(150000):strip_icc()/GettyImages-1171915609-b5823af26fbe42a08125a6a9cd87888b.jpg)

How the Bank of Japan's Interest Rate Hike Could Impact US Investors

Are Negative Rates a Natural Historical Development?

Traders Bet a Ueda-Led BOJ Will Soon End Yield Curve Control - Bloomberg

Inversion Watch: Dancing the Global “Yield Curve” Tango?

Yield Curve Control In The United States, 1942 to 1951 - Federal Reserve Bank of Chicago

What BOJ Ending Yield-Curve Control Could Mean for Global Bonds and Japanese Equities - CME Group

Japan Faces Down Market Testing Limits of Yield Curve Control - Bloomberg

Japan's Experience with Yield Curve Control - Liberty Street Economics

CNBC explains: The Bank of Japan 'yield curve control

A note on modelling yield curve control: A target-zone approach - ScienceDirect

The Fed Tackles Kalecki Institute for New Economic Thinking